The US stock market just had its best week of 2023 as Treasury yields plunged, fueling hopes of an early “Santa rally” to end the year. Scrooges say there’s still plenty in the way.

“I don’t believe in this recovery and I don’t think we’re going to have a rally at the end of the year,” Jason Hsu, chief investment officer at Rayliant, said in a phone interview.

To see: Dow posts best week since October 2022 as stocks rise on soft jobs report

Doubters point to early signs of a cooling labor market, which is currently reinforcing market expectations that the Federal Reserve is done raising rates, and is still likely to result in an outright slowdown that will hit consumer spending and corporate profits in the coming years. will affect quarters.

Bulls counter that consumers are holding up well after remarkably strong third-quarter gross domestic product growth that defied economists’ predictions that the U.S. would now be in recession. Consumer spending has remained robust, increasing 4% between July and September.

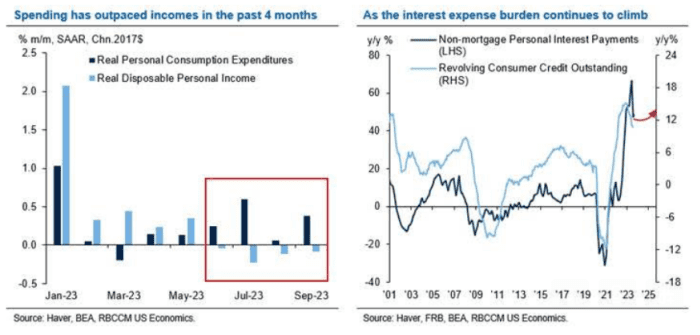

Consumer credit is where bearish investors see problems arising. “Data shows that consumers are short on credit,” Hsu said.

Consumers, previously burdened by pandemic stimulus payments, have become increasingly reliant on credit cards to boost their spending. Revolving credit as a share of personal spending is below pre-coronavirus levels, but the trend is “concerning,” Michael Reid, U.S. economist at RBC Capital Markets, said in a note.

Keywords: Target’s CEO says consumers are cutting back, even on food spending

Personal interest payments as a percentage of disposable income reached 2.7% in September and will continue to rise as federal student loan payments resume, Reid said. As monthly interest payments rise, consumers will need to save further to maintain current spending levels (see charts below).

RBC Capital Markets

“With little room for further declines in savings, the current path is not sustainable,” Reid said.

Economists will keep an eye on the Fed’s Nov. 7 consumer credit report for September.

To see: Spending like crazy? Struggling between paydays? Consumers are sending mixed signals in the run-up to the holidays

Most of the third quarter earnings reporting season is now in the rearview mirror. Gloomy investors focused on weak expectations around the potential for a slower economy.

And during the month of October, analysts cut fourth-quarter earnings per share estimates by a larger margin than average, according to John Butters, senior earnings analyst at FactSet.

Bottom-up fourth-quarter earnings per share estimates fell 3.9% from September 30 to October 31, he said. Analysts typically lower the bar during the first month of a quarter, but not as aggressively. Butters noted that the average drop in earnings expectations in the first month of a quarter averaged 1.9% over the past five years and 1.8% over the past 10 years.

A hurt consumer likely means disappointment is coming on the earnings front in the coming quarters, Hsu said, even as executives try to steer investors toward a “hard landing.”

So what caused the stock to have a great week? Just as a rapid rise in long-term Treasury yields was the main driver of the stock market’s decline from its 2023 high in late July, a sharp decline in yields last week gave stocks room to pull back .

After briefly trading above 5% last week for the first time since 2007, 10-year Treasury yields BX:TMUBMUSD10Y fell 28.9 basis points this week, marking the biggest weekly drop since the period ended March 17 .

It’s been one positive catalyst after another for bond bulls this past week. The U.S. Treasury on Tuesday laid out plans for less Treasury issuance at the long end of the yield curve than expected, and employment data, particularly Friday’s jobs report, showed some signs that a robust labor market could see some early signs of cooling show.

The big event happened on Wednesday, when the Fed, as expected, left rates unchanged and Chairman Jerome Powell left the door open to another rate hike, but did not commit to it. That led investors to largely declare that the Fed is done raising rates — an assumption that some investors say has a significant chance of proving premature.

It was a backdrop that allowed stocks to stage a big rebound a week after the S&P 500 SPX and Nasdaq Composite COMP corrected — down 10% from their 2023 highs. The Dow Jones Industrial Average DJIA rose last week up 5.1%, the biggest gain since the week ending October 28, 2022. The S&P 500 SPX rose 5.5% and the Nasdaq advanced 6.6% – their biggest weekly gains since November of last year.

The previously nervous bulls now see a clear path for a year-end rally.

November and December were the best two-month period on the calendar from a historical perspective, with an average gain of 3% and positive performance 75% of the time, Mark Hackett, head of investment research at Nationwide, said in a note.

Also, the market’s “relief rally” had “some notable echoes of the market bottom a year ago, with extreme weakness in momentum and sentiment indicators,” Hackett wrote. “The resilient macro environment, strong seasonality and improved valuations should provide tailwinds through the end of the year.”

Technical analysts said the market’s rebound, particularly Thursday’s 1.9% gain by the S&P 500, helped lift the charts. The rebound also came as markets had become significantly oversold and bearish sentiment had become extreme, which could be contrarian catalysts for a recovery.

However, more work needs to be done to dispel the gloom, Adam Turnquist, chief technical analyst at LPL Financial, said in a note Friday.

LPL research

Thursday’s rally pushed the S&P 500 back above the closely watched 200-day moving average at 4,248. That’s a “step in the right direction,” but a close above 4,400 is needed for the index to reverse the emerging downtrend, Turnquist said. He noted that market breadth remained disappointing, with less than half of stocks in the S&P 500 trading above their 200. -daily moving average.