Dividend stocks can be great investments. The best ones generate passive income and provide some share price appreciation.

However, stocks with a high dividend yield can be a trap. The payouts may not be sustainable, which could cause investors to see their income and the value of the shares decline. Reliance on medical properties (NYSE: MPW) And Brandywine Realty Trust (NYSE:BDN) currently look like potential dividend traps, according to a number of Fool.com contributors. This is why they think investors should avoid them like the plague this month.

This hospital owner could be a revenue trap

Marc Report (Trust on medical properties): Medical Properties Trust is one of the world’s largest private owners of hospitals and similar properties, with 444 properties and approximately 44,000 licensed beds in 10 countries.

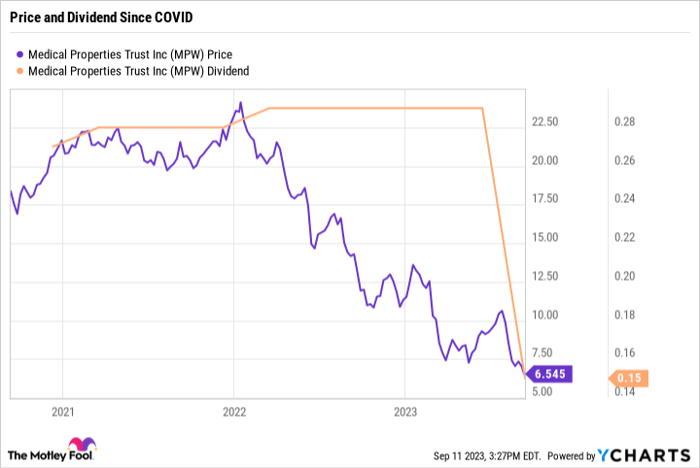

The Birmingham, Alabama-based company is also a Real Estate Investment Trust (REIT), which is required by tax law to pay out at least 90% of its taxable income as dividends, and has done so reliably for decades. That $0.15 per quarter dividend is currently good for a yield of as much as 9% at the share price of $6.54 earlier this week.

It could also be a yield trap. As expected, MPT recently cut its dividend nearly in half, and the company remains embroiled in highly publicized financial struggles as it tries to right a sinking ship.

MPW data by YCharts

The issues are complex and significant, including high levels of debt from acquisitions and some key tenants struggling as they continue to recover financially from the pandemic. It didn’t help when MPT’s practice of financially supporting its operators hit a major snag when California regulators halted such a deal this summer.

MPT has sold some of its properties to help reduce debt, but that also reduces cash flow. The market is not impressed. MPT shares hit an all-time high of around $21 in January 2022 before the current plunge, as shown in the preceding chart. Has the bottom been reached?

The company owns a lot of properties in a very vital sector, and that opportunity always remains. But why get caught up in it now when there might be better alternatives? I used to own MPT shares, and now I can again. But the time doesn’t seem right yet.

A reduction in benefits appears imminent

Matt DiLallo (Brandywine Realty Trust): Brandywine Realty Trust pays an eye-popping dividend that yields more than 15% at the recent share price. however, the office REITs payout hangs by a thread.

The company expects the dividend payout ratio this year to be between 90% and 100% of cash available for distribution. So it is not keeping much money back to finance its development and redevelopment projects. That forces the company to be creative to finance new investments.

It recently sold an office building in Austin, Texas, for $53.3 million. It also took out a construction loan for $50 million. These transactions help bridge the capital plan gap between cash sources and needs.

However, financing the capital plan is only one of the problems. Brandywine also has future debts it needs to address. The next one has a $350 million maturity in October 2024. While the company has time to refinance this debt, it will likely pay a much higher rate. For example, at the end of last year it was able to refinance $350 million in debt maturing in 2023. The problem was that the 7.55% interest on the new 2028 notes was much higher than the 3.95% interest on the maturing debt.

Future debt maturities are likely to increase the company’s interest expense, reducing cash flow. While Brandywine has a number of development projects that should generate rental income as they come online, it faces headwinds in occupancy rates and rents at older properties.

These factors all carry the risk of a dividend cut. Brandywine’s management team noted during the second quarter conference call that their board is keeping a close eye on the dividend. It’s looking increasingly likely that the company will cut its payout, which could happen as early as the current quarter. Given this and all other headwinds, investors should avoid this office REIT.

10 stocks we like better than Medical Properties Trust

If our analyst team has a stock tip, it could be worth listening to. The newsletter they have been publishing for more than ten years, Motley Fool stock advisorhas tripled the market.*

They just revealed what they believe are the ten best stocks for investors to buy right now… and Medical Properties Trust wasn’t one of them! That’s right: They think these 10 stocks are even better buys.

View the 10 stocks

*Stock Advisor returns September 11, 2023

Marc Rapport has no position in the mentioned shares. Matthew DiLallo holds positions in Medical Properties Trust and has the following options: Short January 2024 puts $8 on Medical Properties Trust. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.